I recently had the opportunity to visit with several folks from Assent Inc. for a sponsored podcast series entitled Supply Chain and ESG – What You Need to Know. We discussed: ESG drivers with Jared Connors and James Calder; UFLPA, Supply Chain and ESG with Travis Miller and Jamie Wallisch; the New World of Product Compliance and ESG, with Cally Edgren and Devin O’Herron; Emissions Reporting Strategies with Devin O’Herron and Jared Connors; and Responsible Minerals, Supply Chain and ESG, with Jared Connors and Daniel Zamora. Today, we consider a Scope 3 emissions reporting strategy.

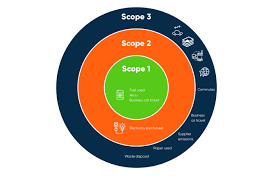

We began with a discussion of the requirements for emissions reporting. There are three Scope levels within the emissions reporting strategy. Scope 1 and 2 are those emissions that are owned or controlled by a company, whereas Scope 3 emissions are a consequence of the activities of the company but occur from sources not owned or controlled by it. Connors provided some examples of each Scope, “Scope 1 is such things as your own vehicle fleets or things you are doing around your facility. Scope 2 is purchases such as heat or electricity for your facility, such as from your municipal power source. Scope 3 is all those variables outside your four walls.”

Connors went on to note, “This makes Scope 3 the most important of the three Scope emissions reporting, because it is so broad. It even includes things like employee travel. The most important aspect of Scope 3 is purchased goods, which has a very large impact on organizations that may not necessarily take in raw materials and directly manufacture from fabrication of those raw materials into a finished goods. Even if your organization designs products and influences those products, you typically will obtain your raw materials components through your supply chain. So purchased goods or supply chain is a very huge impact on the overall emission strategy for companies.”

O’Herron pointed to a recent Accenture study which estimated that Scope 3 emissions are typically 11 times larger than an organization’s Scope 1 and 2 emissions combined. With the increasing use of carbon taxes, and as they progress as a key tool, “the overall mission strategy frankly needs to start accounting for Scope 3.” But it is not simply risks but also opportunities, “because when it comes to Scope 3 emissions in particular, as we think about things like carbon taxes, risk in terms of risk, if you don’t understand what exactly that applies to your organization, you are missing a big opportunity.”

He further cautioned that while the conversation today is dominated by carbon, there may well be other minerals which fall under regulatory ambit. Moreover, there are other environmental factors at play, such waste management, recycled content in products, water usage. All of these additional costs that have not been traditionally quantified and accounted for when thinking about the product life cycle and design of the product. He stated, “when we are talking about Scope 3, in a broader context of just carbon, it’s about broadening the measure of impact burn closer to understanding and identifying the truthful cost of how we provision ourselves today.”

The bottom line is that organizations need to get a handle on their total emissions footprint, which includes what they are collecting from their suppliers upstream, their purchased goods or services, and those in Scope 3 emissions. You cannot manage what you do not measure. This means the “idea of diving into these details, has gained such relevancy and traction in the market.” It is providing a common language and identifying these common topics to focus on in terms of getting that information.

This is a big part of the overall strategy, the data collection at each level in the supply chain and how we may interact with our Tier 1 suppliers, but the disclosure that we get from them, there should be policies, procedures and programs around also creating transparency with their upstream suppliers. Connors concluded, “they have an element of pass down accountability as the phrase was coined so many years ago. I actually try to think of it as pass up accountability, because we are thinking about our supply chain upstream and what we need to collect from those organizations in order to meet the expectations of these regulatory pressures or these market disclosure requirements to create and promote transparency, not only in my operations, my four walls, but upstream of me as well.”

Please plan to join us tomorrow for our final post in this series, on responsible minerals, supply chain and ESG.

To listen to the podcast this blog post is based upon, click here.