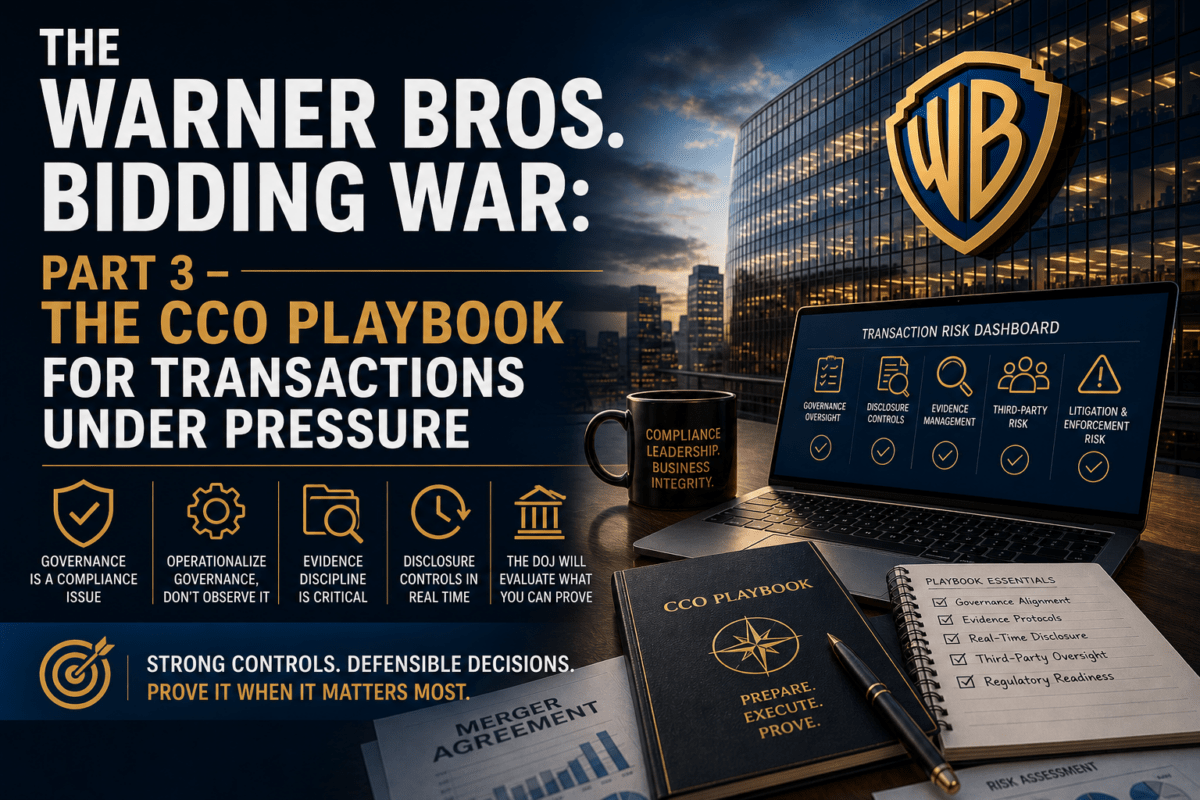

The Warner Bros. Bidding War: Part 3 – The CCO Playbook for Transactions Under Pressure

The Warner Bros. (WBD) bidding war is not simply a Board story. It is a compliance operating model test. When a superior proposal emerges, the Chief Compliance Officer (CCO) must move from program design to execution discipline. Today, we conclude our short review of the Warner Bros./Netflix/Paramount dance and sale by considering lessons for the compliance professional.

In Part 1, we focused on the deal mechanics that led Warner Bros. Discovery to move from an agreed transaction with Netflix to a superior proposal from Paramount Skydance. In Part 2, the focus shifted to Board governance and fiduciary duty. This final post, Post 3, answers the operational question. What must the Chief Compliance Officer do when the process accelerates and governance must be proven in real time?

The answer is grounded in the DOJ’s Evaluation of Corporate Compliance Programs (ECCP). The core question remains constant. Is the program working in practice? A live transaction provides the answer.

Move Compliance Into the Transaction Control Room

Too many compliance functions treat M&A as a legal and financial activity. That approach fails when the transaction becomes contested. Once a superior proposal is identified, the compliance function must:

- Participate in transaction governance meetings

- Map control risks across disclosure, communications, and decision-making

- Establish escalation pathways for new information

This is consistent with the expectations embedded in the DOJ’s Corporate Enforcement Policy, which rewards companies that demonstrate real-time awareness, escalation, and action. A compliance function that is not present during the decision-making process cannot later demonstrate that controls were effective.

Build and Execute an Evidence Protocol

The most significant compliance failure point in transactions is not misconduct. It is the absence of a reliable evidentiary record. In the WBD process, multiple streams of information were created simultaneously:

- Board materials

- Banker communications

- Draft proposals and revisions

- Internal analyses and emails

The CCO must ensure that the company has an evidence-based protocol that includes:

- Centralized collection of transaction-related materials

- Defined custodians for document integrity

- Time-stamped records of key decisions and communications

Under the DOJ’s framework, this directly ties to the question of whether the company can demonstrate effectiveness through data and documentation. If the company cannot reconstruct its decision-making process, it cannot defend it.

Treat Disclosure Controls as a Real-Time Compliance System

Post 2 emphasized that disclosure is a governance issue. For the CCO, it is a control system. The compliance function should validate that:

- The disclosure committee is activated and functioning continuously

- There is a clear trigger matrix for Form 8-K filings and proxy updates

- All external communications are coordinated and controlled

This is not theoretical. In a contested transaction, the volume and speed of information create a risk of selective disclosure, inconsistent messaging, or delayed filings. The CCO must ensure that disclosure controls meet the same standard as financial controls. They must be tested, documented, and operational.

Control Third-Party and Advisor Risk

Transactions introduce intense third-party engagement. Investment banks, legal advisors, consultants, and communications firms all operate at speed. In the WBD scenario, third-party actions included:

- Structuring revised proposals

- Communicating deal terms

- Interacting with market participants

The CCO must ensure:

- Clear protocols for third-party communications

- Defined boundaries on who can speak on behalf of the company

- Documentation of all material third-party interactions

This aligns with long-standing expectations under the Foreign Corrupt Practices Act (FCPA) and the broader third-party risk principles embedded in compliance programs. Even in a domestic transaction, third-party risk remains a control issue.

Align Governance With Internal Controls Frameworks

The events described in Parts 1 and 2 map directly onto internal control frameworks such as the COSO Internal Controls Framework. For the CCO, this means:

- Control Environment: Tone at the top regarding disciplined decision-making

- Risk Assessment: Identification of disclosure, litigation, and regulatory risks

- Control Activities: Implementation of approval processes and documentation protocols

- Information and Communication: Real-time disclosure and coordination

- Monitoring: Ongoing review of transaction-related controls

This mapping is not academic. It is how the company demonstrates that governance is structured, repeatable, and effective.

Prepare for Day Two Risk

The transaction does not end with signing or closing. It creates a new risk profile. The CCO must plan for:

- Integration of compliance programs across entities

- Review of legacy decisions made during the transaction process

- Preservation of records for litigation or regulatory review

This is where the DOJ’s focus on continuous improvement becomes critical. The company must show that it learns from the transaction and strengthens its program.

Connecting the Lessons Across the Series

Part 1 showed that deal terms, including termination fees and superior proposal mechanics, can change outcomes. Part 2 demonstrated that the Board must govern those changes through documented, disciplined processes. In Part 3, we demonstrated the connections between the two. The compliance function is the mechanism that allows the company to prove that governance worked. Without compliance execution, governance is an assertion. With compliance execution, governance becomes evidence.

Practical Action Steps for CCOs

- Embed compliance into the transaction governance structure at the outset of any deal.

- Implement an evidence protocol that captures all material transaction activity in real time.

- Test disclosure controls under accelerated conditions, including mock 8-K scenarios.

- Define and enforce third-party communication protocols.

- Map transaction governance to COSO and DOJ ECCP requirements before a contested situation arises.

Questions for the CCO

- If a regulator requested the full decision record tomorrow, could the company produce it?

- Are disclosure controls capable of operating continuously under transaction pressure?

- Is there a single source of truth for transaction-related documentation?

- Are third-party interactions fully documented and controlled?

- Has the compliance program been stress-tested in a high-speed governance scenario?

Final Thoughts

The Warner Bros. Discovery bidding war is not unique. What is unique is how clearly it illustrates the modern role of the Chief Compliance Officer. Compliance is no longer limited to preventing misconduct. It is responsible for enabling the company to act, decide, and disclose with integrity under pressure and then prove it. That is the standard set by the DOJ. That is the expectation of Boards. And that is the future of the compliance profession.